Anduril Stock: Everything Investors Need to Know Before This Defense Tech Giant Goes Public

If you’ve spent any time scrolling through financial news over the past year, you’ve probably noticed a recurring theme: defense technology is having a moment, and one name keeps popping up more than almost any other. Anduril stock has become one of the most searched, most speculated-about, and most misunderstood topics in the investing world right now. People want in. The problem is that getting in isn’t as simple as opening a brokerage app and typing in a ticker symbol.

This company has gone from a scrappy startup founded by a 24-year-old virtual reality wunderkind to a defense powerhouse valued in the tens of billions of dollars, all in less than a decade. Along the way, it has landed contracts that would make legacy defense contractors nervous, built manufacturing facilities the size of small cities, and attracted investment from some of the biggest names in venture capital. Naturally, retail investors want a piece of the action. But here’s the catch that trips up almost everyone searching for this topic: there is no public Anduril stock ticker you can buy today. Not on the NYSE, not on Nasdaq, nowhere.

That doesn’t mean the conversation ends there, though. Far from it. There’s a whole ecosystem of pre-IPO markets, secondary share transactions, and speculation about a future public listing that makes this one of the more fascinating stories in modern investing. In this article, we’re going to walk through everything that matters: where the company actually stands today, how its valuation has ballooned over the years, what’s driving that growth, the risks nobody talks about enough, and what a potential public offering might eventually look like. Whether you’re a curious beginner just hearing about this company for the first time or a seasoned investor tracking pre-IPO opportunities, there’s a lot of ground to cover here.

What Is Anduril and Why Everyone’s Talking About Anduril Stock

Anduril Industries was founded in 2017 by Palmer Luckey, the same entrepreneur who built and sold Oculus VR to Facebook years earlier. Rather than retire comfortably after that windfall, Luckey pivoted hard into defense technology, betting that the future of military hardware would look less like tanks and battleships and more like software-defined autonomous systems working in concert. That bet has paid off in ways that even early believers probably didn’t expect, and it’s the entire reason there’s now so much chatter around Anduril stock.

The company’s foundational product is Lattice, an AI-powered software platform designed to fuse sensor data from radars, cameras, drones, and other hardware into a single operational picture. Think of it as the nervous system connecting a battlefield’s worth of autonomous eyes and ears. Instead of a soldier staring at a dozen separate screens trying to piece together what’s happening, Lattice does the synthesis automatically, flagging threats and coordinating responses across air, land, sea, and even underwater domains. That software-first approach is a genuine departure from how traditional defense contractors have historically operated, and it’s a big part of why investors are so eager to get exposure to Anduril stock before it potentially hits public markets.

Beyond software, Anduril has built an increasingly diverse hardware portfolio. It makes autonomous underwater vehicles, counter-drone systems, solid rocket motors, and the Fury autonomous combat aircraft. It has also made a habit of acquiring smaller specialized companies to bring critical technology in-house rather than relying on outside suppliers, a strategy that mirrors what companies like SpaceX did in the aerospace world by vertically integrating manufacturing. This combination of ambitious software, expanding hardware capability, and aggressive acquisitions has turned Anduril into something genuinely unusual in the defense sector: a company that behaves like a Silicon Valley tech startup while competing directly against century-old defense primes for massive government contracts.

The Current Status of Anduril Stock: Why You Can’t Buy It on the Open Market

Here’s the plain truth that a lot of headlines gloss over: Anduril stock does not trade on any public stock exchange. The company remains privately held, which means its shares are not available through ordinary brokerage accounts the way you’d buy shares of Apple or Boeing. Anduril’s own investor relations page makes this explicit, stating plainly that the company is privately held and offering guidance about fraudulent investment schemes that sometimes target people looking for a way in.

This distinction matters enormously because it shapes everything else in this conversation. When people search for Anduril stock, they’re often picturing a ticker symbol they can punch into a trading app. What actually exists is a private company whose shares are owned by founders, employees, and a rotating cast of institutional investors including major venture capital firms. Any exposure retail or accredited investors get to Anduril stock right now comes exclusively through secondary market platforms that facilitate private share transactions, and even then, access is typically restricted to accredited investors who meet specific income or net worth thresholds set by securities regulators.

Several platforms have emerged to serve this niche, including Forge Global, EquityZen, and Nasdaq Private Market. These platforms track what’s often called a “Forge Price” or “NPM price,” which is essentially an estimated valuation based on recent private transactions, funding round data, and market sentiment rather than a live, continuously trading price like you’d see on a public exchange. As of mid-2026, that Forge Price for Anduril has been reported around $115 per share, implying a valuation north of $100 billion in secondary market activity, though these figures should be taken as informed estimates rather than hard, verified numbers, since private company pricing lacks the transparency of public markets. Nasdaq Private Market has separately estimated the price closer to $109 per share based on its own proprietary model incorporating multiple market signals.

Anduril’s Valuation History: A Rocket Ship by Any Measure

If you want to understand why so many people are fixated on Anduril stock, you just need to look at the trajectory of its valuation over time. Few companies in any sector, let alone defense, have seen this kind of exponential climb in such a short window.

The numbers tell a remarkable story. Anduril’s very first seed round back in 2017 valued the company at roughly $88 million, a figure that seems almost quaint compared to where things stand now. By 2022, the company had raised close to $1.5 billion in a Series E round that pushed its valuation to $8.48 billion. Two years later, in 2024, another roughly $1.5 billion raise brought the valuation to $14 billion, with Fidelity joining as an investor, a signal that mainstream institutional money was starting to take serious notice of this defense upstart.

Then things really accelerated. In early 2025, a Series G round led by Founders Fund doubled the valuation again to $28 billion. And then came the headline-grabbing moment: in the spring of 2026, Anduril closed a Series H round, raising a reported $5 billion at a $61 billion valuation, more than double its previous mark. That round was led by Thrive Capital and Andreessen Horowitz, two of the most influential venture firms in the technology world. Some reporting has pointed to an even larger figure, with certain sources citing a $2.5 billion raise pushing valuation past $61 billion around the same period, reflecting how quickly and fluidly these numbers have been shifting as new capital pours in.

By mid-2026, secondary market pricing had pushed implied valuations even higher, with some private market indices suggesting figures north of $100 billion based on trading activity on platforms like Forge. That’s a staggering climb from a defense tech startup with roots in a garage-style beginning less than a decade earlier. For context on just how fast this has moved, Forbes has pointed out that the $61 billion valuation from the Series H round equated to roughly 28 times trailing revenue, a multiple far above what traditional defense contractors like Lockheed Martin typically command in public markets, where investors tend to prize steady, predictable cash flows over explosive growth.

That last point deserves some unpacking because it goes to the heart of what makes Anduril stock such a unique proposition. Traditional defense companies trade more like utility stocks: reliable, unglamorous, valued for consistency rather than growth. Anduril, on the other hand, is being valued more like a high-growth AI or software company, which brings both extraordinary upside potential and heightened risk if growth expectations aren’t met.

How to Buy Anduril Stock Before It Goes Public

Given that Anduril stock isn’t available on public exchanges, the natural next question is how anyone actually gets exposure to it today. The answer involves navigating the world of pre-IPO secondary markets, and it’s worth understanding both the opportunity and the limitations before diving in.

The most common route is through specialized platforms designed to connect buyers and sellers of private company shares. Forge Global, EquityZen (a subsidiary of Morgan Stanley), and Nasdaq Private Market are among the most established names in this space. These platforms typically work by matching accredited investors with existing shareholders, often early employees or early-stage investors, who are looking for liquidity before an eventual IPO or acquisition. The mechanics can vary, but generally you’ll need to complete an accredited investor verification process, which usually means demonstrating a certain income level, net worth, or professional financial credential, before you’re even permitted to browse available deals.

Some platforms also offer access through pooled investment vehicles like special purpose vehicles (SPVs) or dedicated funds, which allow investors to gain fractional exposure to Anduril stock without needing to purchase a full block of shares directly from a seller. IPO Club, for instance, has described offering access through vehicles like the “America 2030 Fund” and single-name SPVs specifically targeting defense technology exposure. These structures can lower the minimum investment threshold, but they often come with additional fees and reduced liquidity compared to direct share ownership, so it’s worth reading the fine print carefully.

It’s also worth being realistic about what these secondary transactions represent. Because there’s no centralized, transparent order book the way there is for public stocks, pricing on these platforms is inherently less liquid and can be more volatile in terms of bid-ask spreads. A seller motivated to cash out may accept a lower price than the theoretical market value, while limited supply relative to investor demand can push prices higher during periods of strong sentiment. This supply-demand imbalance has been a recurring theme in reporting on Anduril’s secondary market activity, with strong buy-side interest reflected in elevated bid volume on platforms like Forge even when available shares remain scarce.

One more important caveat: Anduril’s own investor relations materials specifically warn about unauthorized share transfer restrictions and fraudulent investment schemes targeting people eager to buy in before an IPO. This is a real risk in the pre-IPO space generally, not unique to Anduril, but it’s a reminder that anyone considering this route should work only through established, regulated platforms and should never wire funds to unverified intermediaries promising guaranteed access to Anduril stock.

Understanding Anduril’s Business Model and Revenue Growth

To really evaluate whether Anduril stock deserves a place in your portfolio someday, you need to understand how the company actually makes money and how quickly that revenue is growing. This isn’t a company coasting on hype alone; there’s substantial commercial traction behind the valuation numbers.

Anduril reported revenue of approximately $1 billion in 2024, roughly doubling from the prior year. That growth didn’t slow down. By 2025, the company had reportedly generated around $2.2 billion in revenue, more than doubling again year over year. And looking ahead, the company has projected it expects to roughly double revenue once more to approximately $4.3 billion, a trajectory that, if sustained, would put Anduril among the fastest-growing companies in the entire defense and aerospace sector regardless of whether it’s public or private.

That kind of growth doesn’t happen by accident, and it stems directly from Anduril’s unusual business model. Rather than bidding on individual, siloed defense programs the way traditional contractors do, Anduril has positioned itself as a platform provider, selling both software licenses for Lattice and the underlying autonomous hardware that plugs into it. This bundled approach has proven attractive to government buyers looking to modernize and consolidate what has historically been a fragmented, inefficient procurement process spread across dozens of separate vendors and systems.

A great example of this consolidation strategy in action is the massive $20 billion contract Anduril secured from the U.S. Army in 2026. That agreement, potentially spanning ten years, consolidates procurement of the company’s proprietary Lattice AI suite and related hardware, effectively simplifying more than 120 previously fragmented procurement actions into a single unified framework. As one analysis put it, this contract validates Anduril’s software-first approach and positions the company to compete directly with legacy defense contractors for large-scale program management responsibilities that used to be the exclusive domain of companies like Raytheon or General Dynamics.

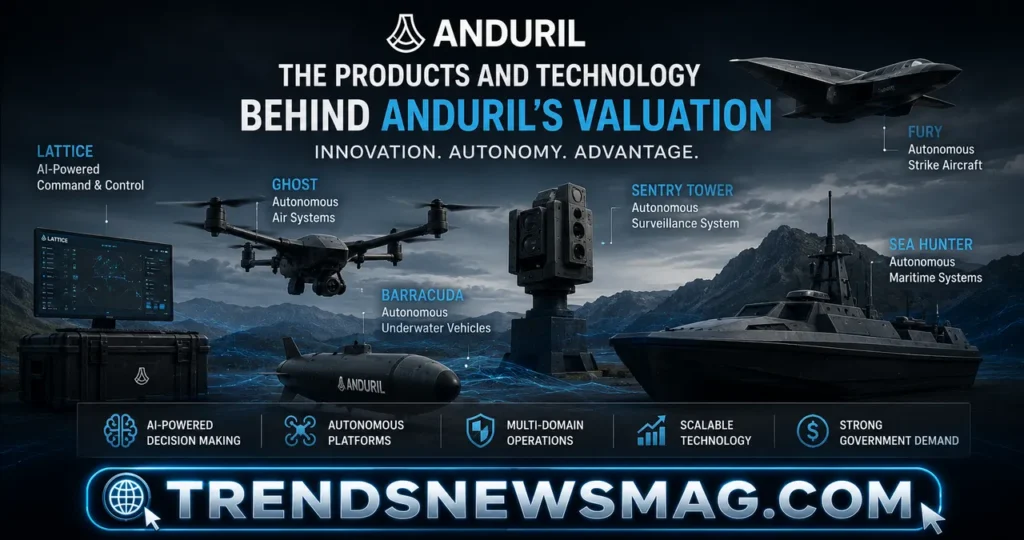

The Products and Technology Behind Anduril’s Valuation

It’s one thing to talk about revenue growth in the abstract, but the actual products driving that growth deserve a closer look, because they explain why investors are so bullish on Anduril stock in the first place.

Lattice remains the crown jewel of the company’s offerings. Described by Anduril as an autonomous sensemaking and command-and-control platform, Lattice serves as the connective tissue for the company’s broader suite of capabilities. It’s designed to ingest data from radar systems, electro-optical sensors, acoustic detectors, and other sources, then use artificial intelligence to identify threats, track objects, and recommend or even automate responses. This is a fundamentally different value proposition than selling a single piece of hardware; it’s selling an operating system for modern warfare, one that can theoretically scale across an entire branch of the military rather than being locked to a single weapons platform.

On the hardware side, the Fury autonomous combat aircraft represents one of Anduril’s most ambitious bets, aiming to provide an affordable, expendable alternative to traditional fighter jets for certain mission profiles. The company has also developed the Dive-LD autonomous underwater vehicle for maritime surveillance and the Omen hover-to-cruise autonomous air vehicle, unveiled in late 2025, which is designed to combine vertical takeoff capability with efficient long-range cruise flight. Counter-drone systems have become an increasingly important product line as well, particularly given how prominently small drones have featured in recent global conflicts, and Anduril has backed that push with contracts including a $200 million agreement with the Marine Corps.

Manufacturing capacity has also become a major strategic focus. The company’s Arsenal-1 facility in Ohio, a 5-million-square-foot autonomous weapons manufacturing complex, represents roughly $1 billion in investment and is expected to create more than 4,000 jobs once production ramps up. Production at Arsenal-1 was targeted to begin in mid-2026. Anduril has also opened a solid rocket motor production facility in Mississippi, with an eventual capacity target of 6,000 motors annually by the end of 2026, addressing a critical bottleneck in the broader U.S. defense industrial base where solid rocket motor supply has struggled to keep pace with demand. There’s even an international manufacturing partnership, the EDGE-Anduril Production Alliance based in the UAE, extending the company’s manufacturing footprint beyond U.S. borders.

Major Government Contracts Powering Anduril’s Growth Story

No discussion of Anduril stock would be complete without digging into the contract wins that have transformed the company from an interesting startup into a genuine force in the defense procurement world. Government contracts are, after all, the lifeblood of any defense company’s revenue, and Anduril’s contract portfolio has grown dramatically in both size and prestige.

Beyond the headline $20 billion Army enterprise contract already mentioned, Anduril has assembled an impressive roster of individual program wins. The company secured a $99.6 million contract for its Next-Generation Command and Control (NGC2) ecosystem in early 2025, along with a $159 million Soldier Borne Mission Command program contract from the U.S. Army in mid-2025. Perhaps most notably, Anduril took over the $22 billion Integrated Visual Augmentation System (IVAS) program that had previously been assigned to Microsoft, a striking vote of confidence from the Pentagon in Anduril’s ability to deliver on one of the most technically demanding and previously troubled programs in recent military procurement history.

Anduril’s presence extends beyond purely military applications, too. The company has deployed multi-domain surveillance systems along U.S. and allied borders under contracts with the Department of Homeland Security, applying its sensor fusion and autonomous detection technology to border security missions. This diversification across mission types, spanning conventional warfighting, homeland security, and even space-adjacent applications through acquisitions like American Infrared Solutions, gives the company multiple avenues for continued government spending even if priorities shift within any single agency or program.

There’s also a notable partnership angle worth mentioning: in December 2024, Anduril announced a collaboration with OpenAI to develop artificial intelligence solutions specifically tailored for national security missions. This kind of partnership underscores how thoroughly intertwined the defense technology and broader artificial intelligence industries have become, and it’s part of why some analysts categorize Anduril less as a traditional defense contractor and more as an AI company that happens to sell into the defense market. That framing matters a lot for how investors should think about Anduril stock, because AI companies and traditional industrial defense companies tend to be valued using very different frameworks and growth assumptions.

Anduril Stock vs. Traditional Defense Contractors: What’s Different

One of the most useful ways to understand the appeal and the risk profile of Anduril stock is to compare it directly against the established players in the defense sector: companies like Lockheed Martin, Northrop Grumman, Raytheon, and General Dynamics. These are the companies that have dominated defense procurement for decades, and Anduril’s entire strategic positioning is built around doing things differently than they do.

Traditional defense primes generally operate on a program-by-program contracting model, bidding on individual weapons systems or platforms and often building custom, purpose-built hardware for each specific program with limited software integration across systems. Their revenue growth tends to be slow and steady, tracking closely with defense budget growth, and their stock valuations reflect that stability, typically trading at modest earnings multiples in the low double digits. Investors buy these stocks for dividends, share buybacks, and defensive characteristics during economic downturns, not for explosive growth potential.

Anduril flips that model on its head. Its software-first philosophy means the company aims to sell a unified platform, Lattice, that can work across many different hardware systems and mission types, creating potential for the kind of recurring software revenue and platform lock-in effects that Silicon Valley investors are accustomed to seeing from companies like Salesforce or Palantir. That’s precisely why Anduril’s private valuation has commanded a revenue multiple many times higher than what public defense contractors receive. It’s being priced like a high-growth technology company rather than an industrial manufacturer, and that pricing philosophy will be put to a real test whenever Anduril stock eventually does become available on public markets, since public market investors tend to demand more transparency and consistency than private markets sometimes require.

There’s also a cultural and operational difference that shouldn’t be underestimated. Anduril has explicitly modeled parts of its manufacturing and operational philosophy on companies like SpaceX, emphasizing speed, vertical integration, and iterative hardware development rather than the slower, more bureaucratic development cycles typical of legacy defense programs. Palmer Luckey has been vocal about wanting to prove the company can execute on ambitious manufacturing goals, particularly around the Arsenal-1 facility, before taking the company public, a sign that leadership is deliberately trying to de-risk the eventual public offering by demonstrating operational credibility first.

Table: Anduril’s Funding Rounds and Valuation Growth

| Funding Round | Approximate Year | Valuation | Notable Investors |

|---|---|---|---|

| Seed Round | 2017 | ~$88 million | Early founders and angel investors |

| Series E | 2022 | ~$8.48 billion | Multiple venture backers |

| Series F | 2024 | ~$14 billion | Fidelity and existing investors |

| Series G | Early 2025 | ~$28-30.5 billion | Founders Fund |

| Series H | 2026 | ~$61 billion | Thrive Capital, Andreessen Horowitz |

| Secondary Market Pricing | Mid-2026 | ~$100+ billion (implied) | Forge, Nasdaq Private Market platforms |

This table illustrates just how dramatically the story has evolved. In under a decade, the company moved from a valuation that wouldn’t even register as a rounding error for major defense contractors to a figure that puts it in the same conversation as some of the largest publicly traded defense companies in the world. Keep in mind that these later-stage figures, particularly the secondary market pricing, represent estimates derived from limited private transactions rather than confirmed, audited valuations, so some caution is warranted when interpreting the most recent numbers.

The Risks Nobody Talks Enough About With Anduril Stock

It’s easy to get swept up in growth numbers and headline contract wins, but any serious evaluation of Anduril stock needs to grapple honestly with the risks involved, because there are several that deserve real attention before anyone commits capital to this space, even through secondary markets.

The most obvious risk is customer concentration. The U.S. government, particularly the Department of Defense and Department of Homeland Security, represents Anduril’s dominant customer base. While government contracts can provide a degree of revenue stability that commercial businesses often lack, they also expose the company to political, budgetary, and procurement risk in ways that diversified commercial companies typically avoid. A change in administration priorities, a defense budget cut, or a shift in procurement strategy could meaningfully impact Anduril’s contract pipeline, and unlike a company selling to thousands of individual commercial customers, there’s no easy way to diversify away from that concentration risk in the near term.

Capital intensity is another underappreciated concern. Building facilities like Arsenal-1 and the Mississippi rocket motor complex requires enormous upfront capital expenditure well before that manufacturing capacity translates into revenue. This is fundamentally different from a pure software business model, where marginal costs of scaling are relatively low. Anduril’s hybrid software-and-hardware approach means it needs continued access to capital, whether through additional funding rounds, government advance payments, or eventually public markets, to keep building out the physical infrastructure its growth targets depend on. As one industry analysis noted, this reliance on a single, cyclical sector introduces a degree of unpredictability that could challenge the company’s operational performance if defense spending priorities shift.

There’s also meaningful regulatory and ethical risk baked into Anduril’s core business. Autonomous weapons systems, AI-enabled targeting technology, and export control compliance are all areas that carry real reputational and legal exposure. Public sentiment around autonomous warfare technology remains contested, and any high-profile controversy, whether involving a malfunction, an export control violation, or public backlash against autonomous weapons more broadly, could create headwinds that don’t typically affect more conventional industrial or software businesses. Investors considering exposure to Anduril stock, even through pre-IPO channels, should factor in this dimension of risk alongside the more conventional financial metrics.

Finally, there’s the straightforward liquidity risk inherent in any pre-IPO investment. Unlike publicly traded stocks that can be bought or sold within seconds during market hours, shares acquired through secondary marketplaces can be difficult to resell, particularly if broader sentiment toward defense technology or private markets cools. There’s no guarantee that Anduril will go public on any particular timeline, or at all; the company could just as easily be acquired, merge with another entity, or simply remain private indefinitely if its current investors are satisfied with the liquidity secondary markets already provide. Anyone buying into pre-IPO Anduril stock through these channels should treat that capital as illiquid for an indefinite period and size their investment accordingly.

When Will Anduril Go Public? The IPO Timeline Question

This is probably the single most searched question connected to Anduril stock, and unfortunately, the honest answer is that nobody outside the company’s boardroom knows for certain. But there are meaningful signals worth examining.

Company leadership has been relatively candid about the general timeline, even if specifics remain elusive. Executive Chairman Trae Stephens stated that while Anduril is not on what he called a “rapid path” to an IPO, the company is actively going through the processes required to prepare for something like that in the medium term. That’s a notably different posture than a company with no public market ambitions at all; it suggests IPO preparation is underway internally even without a committed date.

Founder Palmer Luckey has echoed a similar sentiment, expressing a desire to prove the company can successfully execute on its ambitious manufacturing goals, particularly around the Arsenal-1 facility, before subjecting the business to the scrutiny that comes with public markets. This makes strategic sense: going public prematurely, before demonstrating that massive facilities like Arsenal-1 can actually hit production targets, would expose the company to intense quarterly scrutiny on metrics it might not yet be ready to deliver consistently. Analysts at Forge Global have similarly suggested that a 2026 or 2027 listing is plausible if the Ohio manufacturing facility proceeds as planned and broader IPO market conditions remain relatively favorable.

There’s also a financial logic working against urgency here. The company’s massive Series H raise, bringing in roughly $5 billion in fresh private capital at a $61 billion valuation, significantly reduces any near-term pressure to tap public markets for cash. When a company can raise billions of dollars privately at valuations climbing into the tens of billions, the traditional incentive for going public, namely access to capital, becomes less pressing. Instead, the more likely triggers for an eventual Anduril stock IPO would be some combination of sustained strong public market conditions for growth and defense-adjacent stocks, continued revenue expansion, clearer and more predictable profitability metrics, and a genuine desire among early investors and employees to access liquidity that an IPO would provide more broadly than current secondary market channels can offer.

Until the company actually files an S-1 registration statement with securities regulators, any specific IPO date remains pure speculation, no matter how confidently various financial media outlets frame their predictions. What we can say with more confidence is that the underlying fundamentals, revenue growth, contract wins, and manufacturing buildout, are all trending in a direction consistent with a company preparing itself for eventual public market scrutiny, even if the exact calendar remains uncertain.

Anduril Stock Price Predictions and What Analysts Are Watching

Because there’s no public trading history for Anduril stock, traditional analyst price targets in the way you’d see for an established public company simply don’t exist yet. What does exist is a growing body of speculation, secondary market pricing data, and forward-looking commentary from firms tracking private markets closely.

Morgan Stanley’s defense-tech forecasting has projected the company’s revenue trajectory climbing from roughly $1 billion in 2024 to approximately $2 billion in 2025 and around $4.5 billion by 2026, broadly consistent with the company’s own stated revenue growth targets. If Anduril can sustain anything close to that growth rate into an eventual public listing, it would represent one of the more remarkable revenue growth stories among any major IPO in recent memory, regardless of sector.

Secondary market pricing has already shown meaningful volatility and upward momentum through 2026, with the Forge Price climbing to roughly $115 per share and implied valuations from certain platforms exceeding $100 billion by mid-year, even though the last confirmed primary funding round valuation stood at $61 billion. This gap between the last official primary funding round and elevated secondary market pricing illustrates just how much speculative enthusiasm has built up around the eventual public debut of Anduril stock. It’s worth treating these secondary market figures with some skepticism, though, since they’re based on relatively thin trading volume compared to what a true public market would generate, and prices in illiquid private markets can swing significantly based on just a handful of transactions.

What most serious analysts seem to agree on is that whenever an actual IPO does happen, the pricing conversation will hinge heavily on how public market investors decide to categorize Anduril: as a defense contractor, which would imply a much lower revenue multiple similar to Lockheed Martin or Northrop Grumman, or as a high-growth AI and autonomy platform company, which would justify something closer to the rich multiples the company has commanded in private markets. That classification debate, more than any single financial metric, is likely to be the defining question shaping Anduril’s eventual public stock price and long-term valuation trajectory.

Getting Defense Tech Exposure While Waiting for Anduril Stock

For investors who don’t meet accreditation requirements, don’t want the illiquidity of pre-IPO secondary markets, or simply want to build broader defense sector exposure while waiting to see how the Anduril story unfolds, there are meaningful alternatives worth considering in the meantime.

Established publicly traded defense contractors like Lockheed Martin, Northrop Grumman, and Kratos Defense & Security Solutions offer direct, liquid exposure to the broader defense spending trends that are also benefiting Anduril. These companies won’t deliver the explosive growth potential associated with Anduril’s software-first model, but they provide dividend income, established government relationships, and the kind of stability that comes from decades of operating history, characteristics that Anduril, as a private company with a much shorter track record, simply cannot yet offer public investors. Kratos in particular has drawn comparisons to Anduril given its own focus on unmanned and autonomous systems, making it a reasonable proxy for investors seeking exposure to similar technological themes through an already-public vehicle.

Defense-focused exchange-traded funds represent another avenue worth exploring, offering diversified exposure across multiple defense and aerospace companies rather than concentrating risk in a single name. Since Anduril itself isn’t available through any ETF given its private status, these funds instead provide broader thematic exposure to the same secular trends, rising global defense spending, growing emphasis on autonomous and AI-enabled military systems, and geopolitical tensions driving increased government investment, that are fueling Anduril’s own growth story. Firefly Aerospace, which completed its own IPO in August 2025, represents another interesting comparison point, giving investors a sense of how a newly public space and defense technology company has been received by public markets, potentially offering clues about how Anduril stock might eventually be received when its own listing arrives.

It’s also worth paying attention to companies further down Anduril’s own supply chain or in adjacent niches, since the broader autonomous systems and defense AI ecosystem is expanding well beyond any single company. As one analyst observed regarding the broader climate around defense-adjacent growth companies, “It seems plausible that an Anduril IPO could come in 2026 or 2027 if the Ohio manufacturing facility goes as planned and IPO conditions look relatively strong,” a sentiment that reflects the cautious optimism many market watchers share about this space more broadly, even if specific timing remains genuinely uncertain.

Conclusion: What the Future Holds for Anduril Stock

Pulling all of this together, the story of Anduril stock is really a story about a company that has managed to compress what might normally take multiple decades of gradual defense industry growth into less than ten years. From a modest $88 million seed valuation in 2017 to a private valuation of $61 billion following its 2026 Series H round, with secondary markets pricing the company even higher, Anduril has fundamentally challenged assumptions about how quickly a defense technology company can scale and how investors should value software-first approaches to military procurement.

For now, the honest reality remains that there’s no public Anduril stock ticker to buy, and anyone telling you otherwise either doesn’t understand the current situation or is trying to sell you something questionable. Exposure remains limited to accredited investors through secondary marketplaces like Forge, EquityZen, and Nasdaq Private Market, each carrying its own set of liquidity constraints, pricing uncertainty, and access limitations that ordinary retail investors need to understand before participating. The company’s leadership has signaled genuine interest in an eventual public listing, likely sometime in 2026 or 2027 based on current commentary, but has also been clear that operational execution, particularly around massive manufacturing investments like Arsenal-1, takes priority over rushing toward a public debut.

What makes this story genuinely compelling, beyond the raw valuation numbers, is the broader thesis it represents: that the future of military technology increasingly resembles software and AI more than traditional heavy manufacturing, and that companies willing to bet on that thesis early can capture outsized value as government procurement slowly but surely modernizes. Whether Anduril stock ultimately justifies its lofty private valuation once it faces the harsher, more transparent scrutiny of public markets remains an open question, one that will likely be answered over the next couple of years as the IPO story continues to develop. Until then, patient investors have real alternatives for defense sector exposure, and curious observers have one of the more genuinely fascinating corporate growth stories in modern business to follow along the way.

FAQs

Is Anduril stock available to buy right now?

No, Anduril stock is not currently available for purchase on any public stock exchange because the company remains privately held. The only way to gain exposure is through pre-IPO secondary market platforms such as Forge Global, EquityZen, or Nasdaq Private Market, and even these avenues are typically restricted to accredited investors who meet specific income or net worth requirements. If you come across an offer promising direct, unrestricted access to Anduril stock outside of these established, regulated platforms, treat it with significant skepticism, since Anduril’s own investor relations page has specifically warned about fraudulent schemes targeting eager investors.

What is Anduril’s current valuation?

As of the company’s most recent confirmed primary funding round, a Series H raise completed in 2026, Anduril was valued at approximately $61 billion. However, secondary market pricing on platforms tracking private company valuations has pushed implied figures even higher, with some estimates from mid-2026 suggesting valuations exceeding $100 billion based on recent private share transactions. It’s important to distinguish between the officially confirmed funding round valuation and these secondary market estimates, since the latter are based on more limited trading activity and can be more volatile or speculative in nature.

When will Anduril go public and offer real Anduril stock to retail investors?

There’s no confirmed IPO date at this time, and the company has not filed the necessary registration paperwork with securities regulators. Company leadership, including Executive Chairman Trae Stephens and founder Palmer Luckey, have suggested that going public is a medium-term goal rather than an immediate priority, with some analysts speculating a listing could occur in 2026 or 2027 depending on how manufacturing execution and broader market conditions unfold. Until an S-1 filing actually happens, any specific timeline should be treated as informed speculation rather than a certainty.

Why is Anduril valued so much higher than traditional defense contractors?

Anduril’s valuation reflects the market’s willingness to price it more like a high-growth artificial intelligence and software company rather than a traditional industrial defense manufacturer. Its core Lattice platform is designed to function as a scalable, recurring-revenue software product that can integrate across many different hardware systems, a business model that tends to command significantly higher revenue multiples than the program-by-program contracting approach used by legacy defense primes like Lockheed Martin or Northrop Grumman. Anduril’s rapid revenue growth, roughly doubling year over year in recent periods, further supports this growth-oriented valuation framework, though it also means the company faces higher expectations and greater scrutiny if that growth trajectory were to slow.

What are the biggest risks associated with investing in Anduril stock?

The most significant risks include heavy customer concentration in U.S. government contracts, which exposes the company to political and budgetary shifts; the capital intensity required to fund massive manufacturing facilities like Arsenal-1 before that investment translates into revenue; regulatory and reputational risk tied to autonomous weapons and AI-enabled targeting technology; and the fundamental illiquidity that comes with any pre-IPO investment, since there’s no guarantee of when or whether Anduril will actually complete a public listing. Investors considering any exposure to Anduril stock through secondary markets should weigh these risks carefully against the company’s impressive growth metrics and should be prepared to hold any position for an extended, uncertain period.

Can I get exposure to companies similar to Anduril through public markets today?

Yes, several publicly traded companies offer exposure to similar themes around autonomous systems, defense technology, and AI-enabled military applications. Kratos Defense & Security Solutions is frequently mentioned as a comparable public company given its own focus on unmanned systems, while established primes like Lockheed Martin and Northrop Grumman provide broader, more stable defense sector exposure. Defense-focused exchange-traded funds can also provide diversified exposure to the same secular trends driving Anduril’s growth, without requiring accredited investor status or exposure to the illiquidity risks associated with pre-IPO secondary market transactions.

Trending Today: [45.6 Billion Won to USD]